2023 Bitcoin Outlook

2023 Bitcoin Outlook

At bottom? Likely. Recovering soon? No, patience needed.

Dear subscribers,

Welcome to Bitcoin Onchain, Offchain, and Beyond.

With gloomy global macro conditions driven by the Fed’s quantitative tightening and collapses of FTX, Terra, Genesis, BlockFi and varies “fraudulent” tokens, crypto has seen a brutal and chaotic 2022. The good news is we are likely in the “depression” phase of the market cycle. The bad news is there’s no sign of recovery yet, and we could stay in the “depression” phase for a while with painful drawdowns. Below is a summary for market conditions on December 28th 2022 (BTC current price: $16.7k):

Mid/Long term:

BTC will continue making all-time highs, but likely not in 2023.

Liquidity issues continue and long-term holders are still selling in losses. While many on-chain cycle indicators (eg. realized price) are showing BTC is in the cyclical bottom, on-chain recovering signs are missing. Furthermore, the yield curve has inverted again. With prior yield curve inversions since 1960s all leading to depressions and correlation between BTC and SPX hovering at its all time high level, I would prepare for a bumpy road ahead for the first half of 2023.

Short term:

Bearish

On-chain short-term sentiment remains in the bearish trend, and institutional spot traders remain more bearish compared to retail spot traders. On the Bitcoin futures market, institutional traders (CME) remain bearish for the short term.

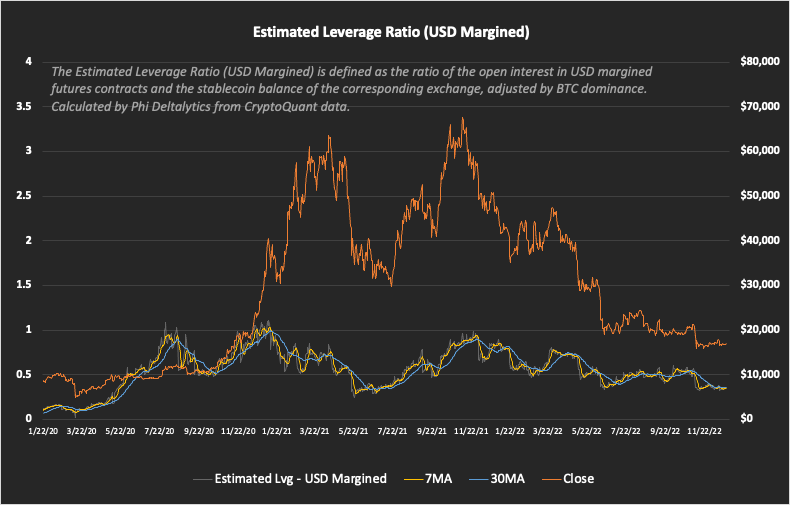

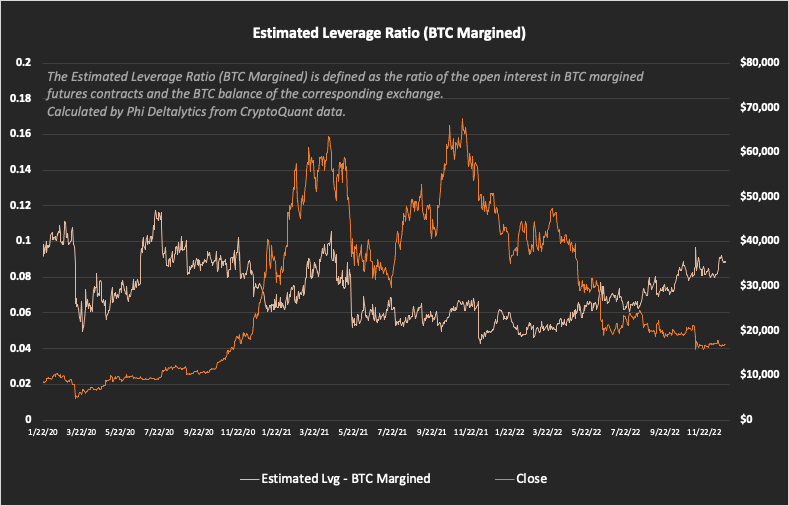

While the estimated leverage ratio for USD-margined Bitcoin futures stays low, the estimated leverage ratio for BTC-margined contracts continued its climb in Q4, 2022. The heated speculations in BTC-margined futures need to quiet down for crypto to truly bottom out.

Happy holidays!

Phi

P.S. If you find the analysis helpful, consider buying me a coffee at 0x646071ED932DCd0019e1EB625947bbbc6a3AF332 (ETH/BSC/Matic/Optimism).

Alarming Macro Conditions

The yield curve has inverted (the interest rate spread between the 10-year Treasury note and the 3-month Treasury bill). With such inversion preceding prior 8 recessions, the global macro condition does not look promising. Furthermore, despite peaked in Q3, the 7.1% U.S. Consumer Price Index (CPI) still remains well above the Federal Reserve’s 2% target. With Q3 real GDP stats better than that of Q1 and Q2, the Fed might tighten the leash in the months to come.

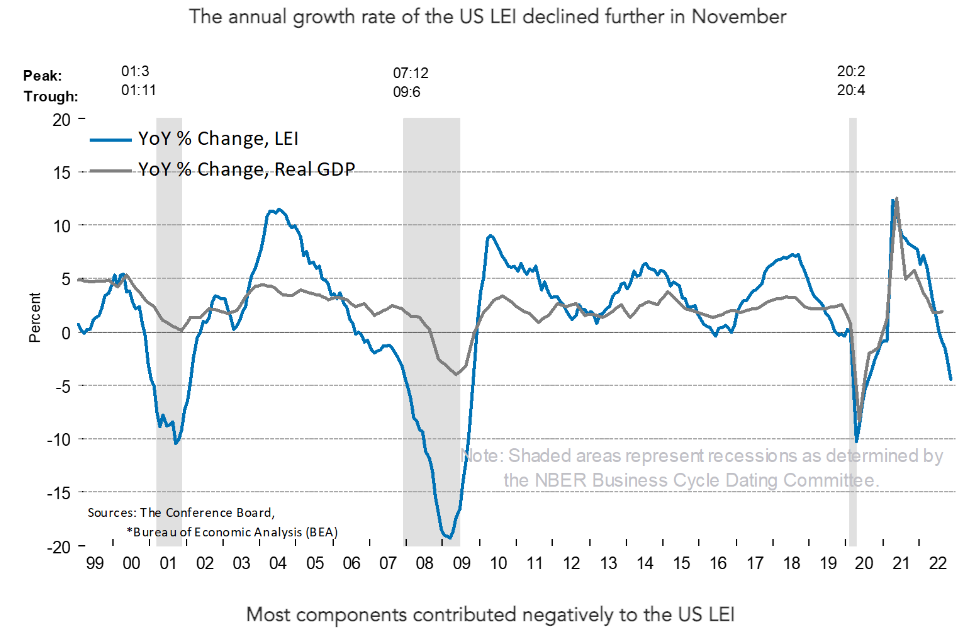

The Leading Economic Index (LEI) for US continued to plummet in November, signaling a potential recession. The LEI is a predictive variable that anticipates (or “leads”) turning points in the business cycle by around 7 months. Shaded areas denote recession periods or economic contractions.

The ten components of The Conference Board Leading Economic Index® for the U.S. include: Average weekly hours in manufacturing; Average weekly initial claims for unemployment insurance; Manufacturers’ new orders for consumer goods and materials; ISM® Index of New Orders; Manufacturers’ new orders for nondefense capital goods excluding aircraft orders; Building permits for new private housing units; S&P 500® Index of Stock Prices; Leading Credit Index™; Interest rate spread (10-year Treasury bonds less federal funds rate); Average consumer expectations for business conditions.

The above chart is from my June newsletter Don’t DCA Yet. It’s worth noting again that in the entire BTC history, most gains were generated in periods of healthy liquidity from either monetary or fiscal policies. Thus, under continued quantitative tightening and a potential recession on the horizon, the upside for Bitcoin is extremely limited.

Cycle Recovering Signs Missing

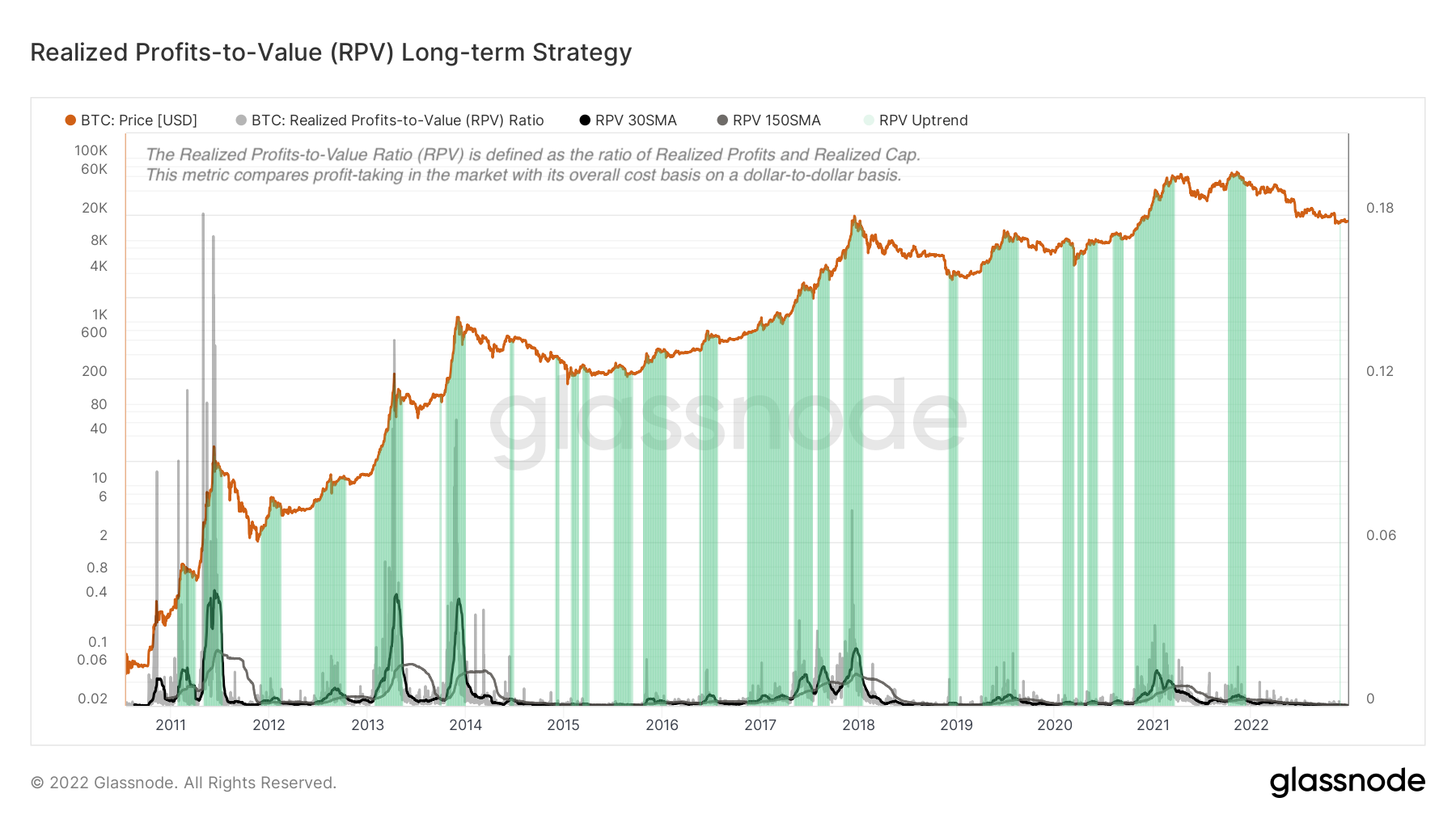

The price of Bitcoin has been under its realized price for more than 100 days. While such periods have led to good historical accumulation levels, these bottoms are also subject to extended periods with large drawdowns. With the crypto market yet to experience a prolonged traditional market recession, the length of the current “depression” bottom could be longer compared to that of prior cycle bottoms.

Cycle recovering signs from on-chain indicators remain missing. Green shaded areas above denote periods of uptrend in the Realized Profits-to-Value (RPV) ratio and the Spent Output profit Ratio (SOPR) respectively. Both long-only strategies have been outperforming Bitcoin and has not shown signs of recovering yet.

Short-term holder Sentiment Remains Bearish

Short-term on-chain participants continue to sell in losses. With price now also testing the on-chain resistance level of 17k, more than normal selling pressure is ahead in the short term.

Institutional Traders Remain Bearish

CME BTC futures spread has stayed significantly negative since October, and the Coinbase premium has stayed mostly negative since May. The two metrics indicate institutional biases in the Bitcoin futures and spot markets. Both metrics have stayed positive in past bull runs.

Quiet USD Margined vs. Heated BTC Margined Futures Trading

While the estimated leverage ratio for USD-margined Bitcoin future contracts stays low, the estimated leverage ratio for BTC-margined contracts continued its climb in Q4, 2022 and is currently close to the level at the 60k top in March 2021. In Bitcoin’s Covid-19 4k bottom and the local 30k bottom between May and July 2021, there were low levels of speculation on the futures trading market with both estimated leverage ratios at low levels. As the “depression” bottom of any market cycle is often marked by low levels of speculation and market activities, the currently heated BTC-margined futures trading likely needs to quiet down for the market to truly bottom out.

Disclaimer

NONE OF THE INFORMATION IS INTENDED AS INVESTMENT ADVICE, AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL, OR AS A RECOMMENDATION, ENDORSEMENT, OR SPONSORSHIP OF ANY SECURITY, GROUP, POOL, OR FUND. IT SHOULD NOT BE ASSUMED THAT THE METHODS, TECHNIQUES, OR INDICATORS PRESENTED IN THIS NEWSLETTER WILL BE PROFITABLE OR THAT THEY WILL NOT RESULT IN LOSSES. PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. THE CONTENT AND ANALYSIS IN THIS NEWSLETTER IS FOR EDUCATIONAL PURPOSES ONLY AND IS NOT INTENDED TO BE AND DOES NOT CONSTITUTE FINANCIAL ADVICE OR ANY OTHER ADVICE. THE INFORMATION PROVIDED IS GENERAL IN NATURE AND NOT SPECIFIC TO YOU. YOU ARE RESPONSIBLE FOR YOUR OWN INVESTMENT RESEARCH AND INVESTMENT DECISIONS.